-

DCAS – our services are continuing

Although we, along with most of you, are no longer funded by Derby City Council, we have received funding from Foundation Derbyshire

Although we, along with most of you, are no longer funded by Derby City Council, we have received funding from Foundation DerbyshireFortunately, we are not totally reliant on external funding to run our services, and we continue to work with up to 150 groups within the Voluntary Sector in Derby and Derbyshire

If you need any help or advice on financial matters, please get in touch with us here

-

Shared Parental Leave and Pay

You may be able to get Shared Parental Leave (SPL) and Statutory Shared Parental Pay (ShPP) if:

You may be able to get Shared Parental Leave (SPL) and Statutory Shared Parental Pay (ShPP) if:- your baby is due on or after 5 April 2015

- you adopt a child on or after 5 April 2015

If you’re eligible for SPL you can use it to take leave in blocks separated by periods of work, instead of taking it all in one go.

To start SPL or ShPP the mother must end her maternity leave (for SPL) or her Maternity Allowance or maternity pay (for ShPP). If she doesn’t get maternity leave (but she ends her Maternity Allowance or pay early) her partner might still get SPL.

Example A mother and her partner are both eligible for SPL and ShPP. The mother ends her maternity leave and pay after 12 weeks, leaving 40 weeks available for SPL and 27 weeks available for ShPP. The parents can choose how to split this.

-

Autumn Training Courses

Having problems managing your finances or querying about employment law?

Having problems managing your finances or querying about employment law?Look no further – we have more training courses coming up in November. More details to follow, but you can book now by emailing us here.

Wednesday 16th November – Financial Management for Voluntary Groups

Wednesday 23rd November – Employment Law

Wednesday 30th November – Budgeting and Cashflow Forecasting

-

CCG Funding Bids Revised Response Date

The Commissioners report that they have received an extremely high number of funding applications, and in order to give full and equal consideration to each bid, they need a little more time.

The Commissioners report that they have received an extremely high number of funding applications, and in order to give full and equal consideration to each bid, they need a little more time.The revised response date in now

Wednesday 21st September 2016

Best wishes to all who have applied.

-

Charity Accounts: Retention of Records

We are often asked how long organisations should retain their financial records, so here is some short guidance:

We are often asked how long organisations should retain their financial records, so here is some short guidance: What are the requirements for all charities?

All charities must:

- keep accounting records – these records (eg cash books, invoices, receipts, Gift Aid records etc) must be retained for at least 6 years (or at least 3 years in the case of charitable companies) – where Gift Aid payments are received records will need to be maintained for 6 years with details of any substantial donors and to identify ‘tainted charity donations’ in accordance with HMRC guidance

-

Student Loan Repayment Plans

Plan types

Plan typesWith effect from the 2016 to 2017 tax year there are 2 plan types for student loan repayments:

- plan 1 with a 2016 to 2017 threshold of £17,495 (£1,457 a month or £336 per week)

- plan 2 with a 2016 to 2017 threshold of £21,000 (£1750 a month or £403 per week)

If you are unsure which plan to use, it is easy to find out by filling in the online survey here

-

Closing a Charity – The Law

Closing a Charity – The Law

Closing a Charity – The LawCharities can close for a number of reasons, such as:

- a merger with another charity

- the original purpose has been met or is no longer relevant, for example treating a disease that has since been eradicated in the area the charity serves

- losing funds or funding

- a lack of members

- becoming a company or charitable incorporated organisation (CIO), which means creating a separate charity

If you do decide to close your charity, you’ll need to tell the Charity Commission if it is a Registered Charity, and clear all its debts and liabilities before you spend its remaining assets on your charity’s purposes. This will include checking if you have any:

- unspent grant money – if so, check if there is any specific agreement with the grantmaker about what to do with it where you are closing the charity

- money from fundraising appeals that haven’t reached their target – if so, check the commission’s guidance on failed appeals to see if you need to return any donations to donors

Further detailed guidance can be found here: https://www.gov.uk/guidance/how-to-close-a-charity

-

Charitable Incorporated Organisations – CIOs

The Charitable Incorporated Organisation – CIO – is a relatively new form of incorporated legal structure that is designed to meet the particular needs of a charity and is only available to charities. A CIO is a corporate body which is not a company incorporated under the Companies Acts; it is therefore not subject to company regulation. Neither its existence nor any charges it creates have to be registered at Companies House.

The Charitable Incorporated Organisation – CIO – is a relatively new form of incorporated legal structure that is designed to meet the particular needs of a charity and is only available to charities. A CIO is a corporate body which is not a company incorporated under the Companies Acts; it is therefore not subject to company regulation. Neither its existence nor any charges it creates have to be registered at Companies House.The corporate structure provided by the CIO meets a demand from the charitable sector for a structure which gives a charity a legal personality of its own, enabling it to conduct business in its own name, rather than in the names of its trustees.

More information can be found on the Government website: https://www.gov.uk/guidance/charity-types-how-to-choose-a-structure

-

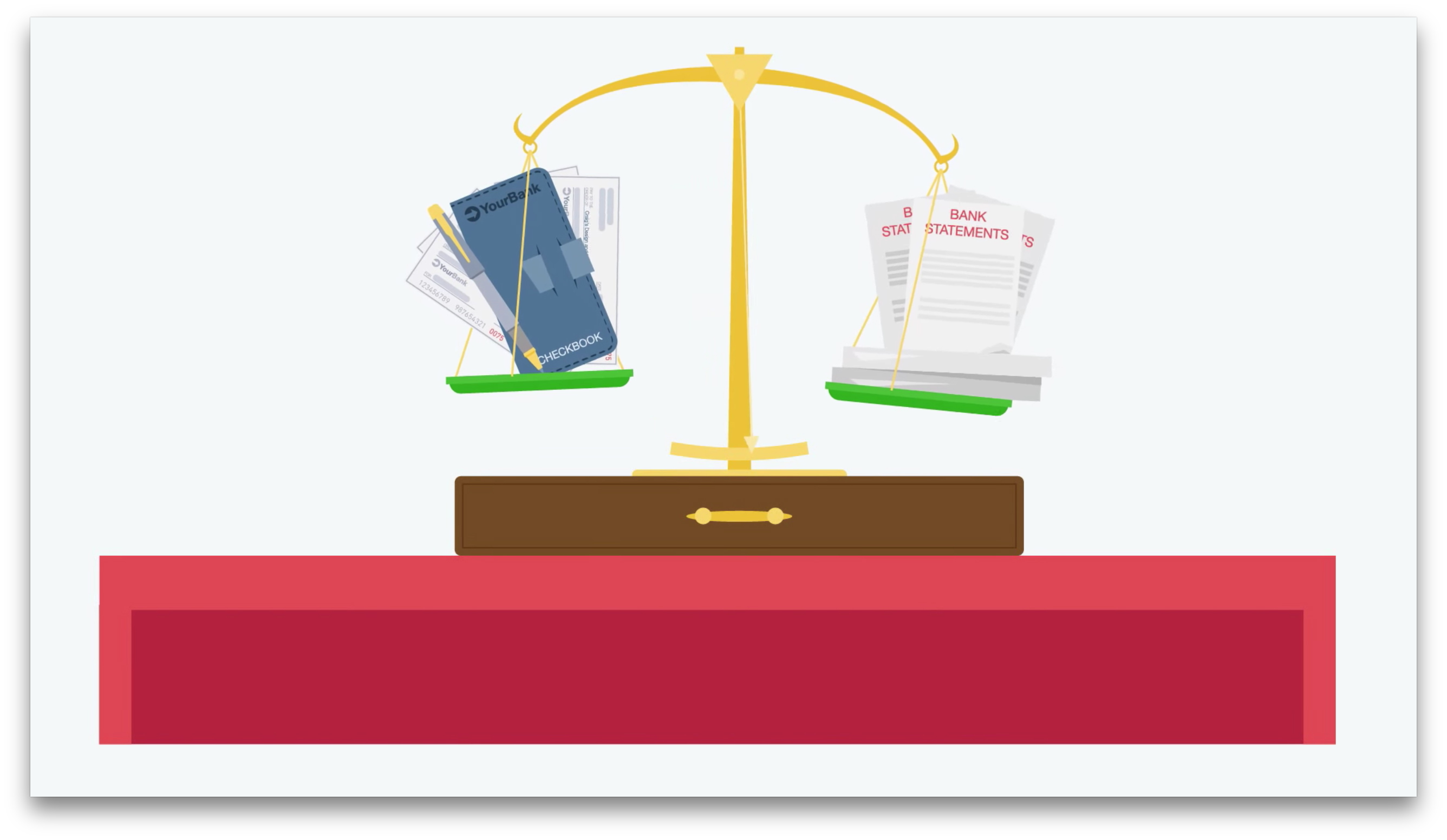

Bank Reconciliation and Statement

Our training manual “The Adventures of Mr Claw in the World of Charity Accounting” – which is being used at professional training courses in Book Keeping – explains Bank Reconciliation and Statement production, and how to implement these procedures in to your organisation’s accounting procedures. Get your copy here

Our training manual “The Adventures of Mr Claw in the World of Charity Accounting” – which is being used at professional training courses in Book Keeping – explains Bank Reconciliation and Statement production, and how to implement these procedures in to your organisation’s accounting procedures. Get your copy here

Here is a brief extract:

The bank reconciliation is the means by which you can give yourself some self-assurance that you have recorded every item of income and expenditure, and that what you have recorded is correct.

When a group has a bank account, a record of the bank transactions is kept in the organisation’s cash book. In addition, the bank also keeps a record of these same transactions and this record is shown on the statement produced by the bank.

There are then two quite separate records of the same transactions.

It is therefore necessary to compare these records regularly to ensure that no errors have arisen, and to explain any differences that there are between the balances, i.e. those shown in the Cash Book and on the bank statement.

This comparison is known as a Bank Reconciliation Statement which is simply a method of explaining any difference that there may be between the two balances.

-

When to Start Paying Sick Pay

When to start paying SSP

When to start paying SSPSSP is paid when the employee is sick for at least 4 days in a row (including non-working days). You start paying SSP from the fourth ‘qualifying day’ (day an employee is normally required to work). The first 3 qualifying days are called ‘waiting days’.

You can’t count a day as a sick day if an employee has worked for a minute or more before they go home sick.

If an employee works a shift that ends the day after it started and becomes sick during the shift or after it has finished, the second day will count as a sick day.

Exception

You don’t usually pay SSP for the first 3 qualifying days unless they’ve been off sick and getting SSP within the last 8 weeks.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.